Future of Retail Payments: 20% Faster Checkout by 2026

Anúncios

The Evolution of Payment Systems: Streamlining US Retail Transactions for a 20% Faster Checkout in 2026

The retail landscape is in a constant state of flux, driven by technological advancements and evolving consumer expectations. In the United States, the quest for efficiency and an unparalleled customer experience has never been more pronounced. A pivotal area of focus for retailers is the payment process. Imagine a world where checkout lines are virtually non-existent, and transactions are completed in mere seconds. This isn’t a distant dream; it’s the near future. Industry experts and technological trends suggest that by 2026, US retail transactions will be, on average, 20% faster than they are today, largely due to significant retail payment innovation. This article will delve into the transformative forces behind this accelerated future, exploring the technologies, strategies, and consumer shifts that are redefining the checkout experience.

Anúncios

The Current State of US Retail Payments: A Foundation for Change

Before we project into the future, it’s essential to understand the current state of retail payment innovation in the US. While credit and debit cards remain dominant, there’s been a noticeable surge in alternative payment methods. Mobile wallets like Apple Pay and Google Pay, once niche, are now commonplace. Contactless payments, accelerated by the pandemic, have seen widespread adoption. However, despite these advancements, bottlenecks still exist. Legacy Point-of-Sale (POS) systems, inconsistent internet connectivity, and the sheer variety of payment options can sometimes create friction at the checkout. The average transaction time, even with modern systems, still leaves room for improvement, and this is precisely where the next wave of retail payment innovation is poised to make its mark.

Consumer patience is a dwindling commodity. Long queues and slow transactions are often cited as major frustrations, leading to abandoned carts and a negative perception of a brand. Retailers recognize this and are actively investing in solutions that promise not just speed, but also security and convenience. The competitive nature of the retail sector further fuels this drive for efficiency. Businesses that can offer a superior, faster checkout experience are more likely to retain customers and attract new ones. This fundamental understanding forms the bedrock upon which the future of faster retail payments is being built.

Anúncios

Key Drivers of Faster Retail Payment Innovation

Achieving a 20% acceleration in checkout speed by 2026 isn’t a singular effort but a confluence of several powerful trends and technological breakthroughs. These drivers are working in tandem to create a more streamlined and efficient payment ecosystem.

1. The Rise of Contactless and Mobile Payments

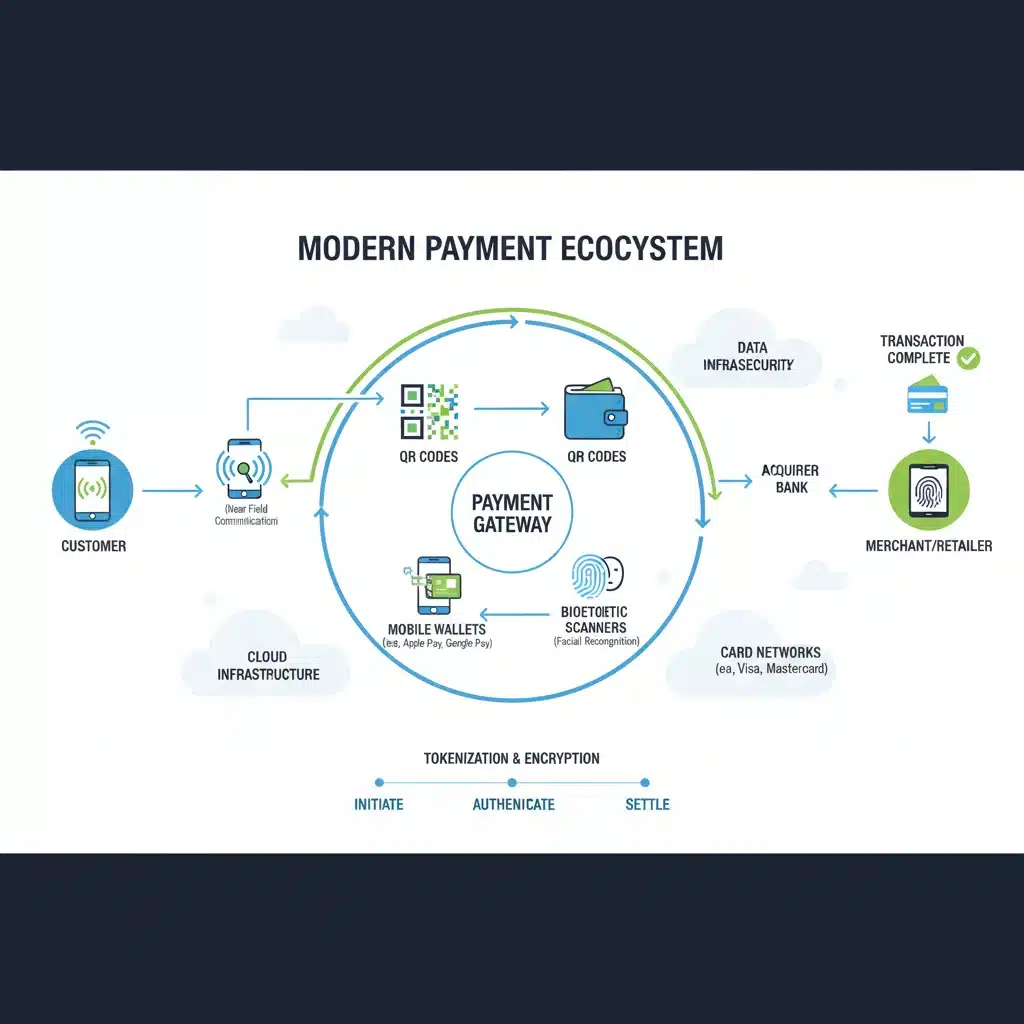

Contactless payments, often facilitated through Near Field Communication (NFC) technology, have significantly reduced transaction times. A simple tap of a card or mobile device eliminates the need for card insertion, PIN entry (in many cases for smaller transactions), or signature. The proliferation of NFC-enabled POS terminals and the increasing comfort consumers have with mobile wallets are key factors here. As more banks issue contactless cards and more smartphones come equipped with NFC, this method will become the default, shaving precious seconds off each transaction. Mobile wallets, in particular, offer an added layer of convenience by storing multiple payment methods, loyalty cards, and even digital receipts, further reducing the physical fumbling at checkout.

2. Enhanced Biometric Authentication

Fingerprint, facial recognition, and even iris scanning are no longer the exclusive domain of science fiction. Biometric authentication is rapidly integrating into payment systems, offering both enhanced security and unparalleled speed. Imagine authenticating a payment with a glance or a thumbprint, bypassing PINs and passwords entirely. This not only makes transactions faster but also more secure, reducing the risk of fraud. As biometric technology becomes more affordable and reliable, its adoption in retail environments will undoubtedly contribute to faster checkout processes.

3. Artificial Intelligence and Machine Learning in Fraud Detection

One of the hidden time sinks in payment processing is fraud detection. Traditional methods can sometimes flag legitimate transactions for review, causing delays. AI and Machine Learning (ML) are revolutionizing this by offering real-time, highly accurate fraud detection. These systems can analyze vast amounts of data in milliseconds, identifying suspicious patterns without interrupting legitimate transactions. This means fewer false positives, fewer manual reviews, and ultimately, faster approvals, contributing significantly to overall retail payment innovation.

4. Cloud-Based POS Systems and Integrated Platforms

Traditional, on-premise POS systems can be slow, clunky, and difficult to update. Cloud-based POS solutions offer a more agile and efficient alternative. They provide real-time data, seamless integration with inventory management, CRM, and other retail systems, and can be updated remotely. This integration reduces errors, streamlines operations, and allows for faster transaction processing. Furthermore, unified commerce platforms that integrate online and offline sales channels simplify the payment experience for both customers and retailers, offering greater flexibility and speed.

5. Self-Checkout and Scan & Go Technologies

While not entirely new, self-checkout technologies are becoming more sophisticated and user-friendly. Beyond traditional self-checkout kiosks, ‘Scan & Go’ apps allow customers to scan items with their smartphones as they shop and pay directly through the app, completely bypassing the checkout line. Amazon Go stores exemplify this with their ‘Just Walk Out’ technology, which uses a combination of computer vision, sensor fusion, and deep learning to detect when products are taken or returned to shelves, automatically charging the customer’s Amazon account. While such advanced systems require significant infrastructure, scaled-down versions are becoming more accessible and are powerful drivers of faster transactions.

6. Open Banking and Instant Payments

Open banking initiatives are paving the way for more direct and immediate payment options. By allowing secure data sharing between banks and third-party providers with customer consent, it fosters innovation in payment services. Instant payment networks, like RTP (Real-Time Payments) in the US, enable funds to be transferred and settled almost immediately. While primarily B2B or P2P currently, the underlying infrastructure and principles of instant payments could eventually filter down to consumer retail, offering immediate confirmation of payment and speeding up the entire transaction lifecycle, further enhancing retail payment innovation.

The Impact of Faster Checkout on the US Retail Landscape

A 20% reduction in checkout time by 2026 will have a profound and multifaceted impact on the US retail sector, benefiting both businesses and consumers.

For Consumers: Enhanced Convenience and Satisfaction

The most immediate and tangible benefit for consumers is the significant reduction in wait times. This translates to a more pleasant shopping experience, less frustration, and more time for other activities. The convenience of quick, seamless payments can also encourage impulse purchases and increase overall spending. Furthermore, increased security through advanced authentication methods builds greater trust in digital payment systems.

For Retailers: Increased Sales and Operational Efficiency

Faster checkouts mean higher throughput. Retailers can process more customers in the same amount of time, leading to increased sales volumes. Reduced queue lengths can also prevent cart abandonment, a significant pain point for many businesses. Operationally, less time spent on manual payment processing frees up staff to focus on customer service, merchandising, or other value-added tasks. The data generated by advanced payment systems also offers valuable insights into consumer behavior, allowing retailers to personalize offers and optimize their operations. This continuous cycle of improvement is a cornerstone of retail payment innovation.

Competitive Advantage

In a highly competitive market, offering a faster and more convenient checkout experience can be a significant differentiator. Retailers who embrace these innovations early will gain a competitive edge, attracting tech-savvy consumers and setting new industry standards. Those who lag behind risk losing market share to more agile competitors.

Challenges and Considerations for Achieving the 20% Acceleration

While the trajectory towards faster retail payments is clear, the journey is not without its challenges. Implementing these advanced systems requires careful planning, significant investment, and overcoming various hurdles.

1. Infrastructure Investment

Upgrading legacy POS systems, installing new hardware for contactless or biometric payments, and ensuring robust network connectivity across all retail locations can be a substantial capital expenditure for many businesses, especially smaller ones. The return on investment, while clear in the long term, might deter some initial adoption.

2. Data Security and Privacy Concerns

As payments become more digital and integrated, the volume of sensitive data handled by retailers increases. Ensuring the highest levels of cybersecurity to protect against breaches and fraud is paramount. Consumers are also increasingly concerned about their data privacy, and retailers must be transparent about how data is collected, stored, and used, complying with regulations like PCI DSS, CCPA, and GDPR.

3. Interoperability and Standardization

The payment ecosystem is fragmented, with numerous providers, technologies, and standards. Achieving seamless interoperability between different systems and ensuring universal acceptance of various payment methods can be complex. Industry-wide standardization efforts are crucial to simplify the integration process and accelerate adoption of retail payment innovation.

4. Consumer Adoption and Education

While many consumers are eager for faster payments, not everyone is equally tech-savvy or comfortable with new technologies. Retailers will need to invest in educating their customers about new payment options, highlighting the benefits of speed, security, and convenience. User-friendly interfaces and clear instructions will be key to driving widespread adoption.

5. Regulatory Landscape

The regulatory environment surrounding payments is constantly evolving. Retailers must stay abreast of new laws and compliance requirements, particularly concerning data privacy, consumer protection, and anti-money laundering (AML). Adapting to these changes can add complexity to payment system implementations.

The Road Ahead: Strategies for Retailers

To capitalize on the coming wave of retail payment innovation and achieve the 20% faster checkout goal, retailers should consider several strategic approaches:

1. Prioritize Mobile and Contactless Infrastructure

Ensure all POS terminals are NFC-enabled and capable of accepting major mobile wallets. Actively promote these payment methods to customers through signage and staff training. This is a foundational step for immediate improvements in checkout speed.

2. Explore Advanced Self-Service Solutions

Beyond traditional self-checkout, investigate ‘Scan & Go’ apps or even more advanced frictionless payment technologies. Pilot these solutions in specific stores to gather feedback and refine the experience before wider rollout. The goal is to empower customers to control their own checkout process, thereby enhancing speed and autonomy.

3. Invest in Robust Cybersecurity Measures

Partner with reputable payment processors and cybersecurity firms to safeguard customer data. Implement end-to-end encryption, tokenization, and multi-factor authentication where appropriate. Building trust through secure transactions is paramount for long-term customer loyalty.

4. Leverage Data Analytics for Optimization

Utilize the data generated by new payment systems to identify bottlenecks, understand peak shopping times, and optimize staffing levels. Data can also inform personalized marketing efforts and inventory management, creating a more efficient overall retail operation.

5. Foster an Omnichannel Payment Experience

Ensure that payment options are consistent and seamless across all sales channels – in-store, online, and mobile. Allow customers to start a purchase in one channel and complete it in another without friction. This holistic approach to payments is crucial for modern retail.

6. Stay Agile and Adaptable

The pace of technological change in payments is rapid. Retailers must remain agile, continuously evaluating new solutions and adapting their strategies to stay ahead of the curve. This involves ongoing research, pilot programs, and a willingness to embrace new paradigms in retail payment innovation.

The Role of Fintech and Payment Processors

Fintech companies and payment processors are at the forefront of driving this retail payment innovation. They are continuously developing new technologies and solutions that make transactions faster, more secure, and more convenient. Partnerships between retailers and these innovators will be critical. Payment processors are not just facilitating transactions; they are becoming strategic partners, offering insights, fraud prevention tools, and integrated platforms that help retailers optimize their entire payment ecosystem. Their expertise in navigating the complex regulatory landscape and implementing cutting-edge security measures is invaluable.

These partnerships often lead to customized solutions tailored to a retailer’s specific needs, whether it’s optimizing for high-volume transactions, integrating loyalty programs directly into the payment flow, or providing advanced analytics tools. The collaboration between retailers and fintech innovators is a powerful engine propelling the industry towards a more efficient and customer-centric future.

Looking Beyond 2026: The Future of Frictionless Retail

While a 20% faster checkout by 2026 is an ambitious yet achievable goal, the journey of retail payment innovation won’t stop there. The ultimate vision is a truly frictionless retail experience where payments are almost invisible. This could involve:

- Embedded Payments: Payments seamlessly integrated into smart shopping carts, smart mirrors, or even smart clothing, where items are automatically detected and charged upon leaving the store.

- Cryptocurrency and Blockchain: While still nascent in mainstream retail, blockchain technology offers the potential for highly secure, transparent, and potentially faster cross-border transactions, and cryptocurrencies could offer alternative payment rails.

- Voice Commerce: Payments initiated and completed through voice commands, integrated with smart home devices or in-car systems.

- Advanced Data Personalization: AI-driven systems that anticipate customer needs and preferences, offering hyper-personalized payment options and promotions in real-time.

These futuristic concepts, while requiring further technological maturation and societal acceptance, underscore the relentless pursuit of convenience and efficiency in retail. The innovations we see today are merely stepping stones towards a retail environment where the act of payment is so integrated and effortless that it becomes an almost subconscious part of the shopping journey.

Conclusion

The US retail sector is on the cusp of a significant transformation in its payment systems. The drive for a 20% faster checkout by 2026 is not merely about speed; it’s about fundamentally enhancing the customer experience, boosting operational efficiency, and securing a competitive edge. Through the widespread adoption of contactless and mobile payments, advanced biometrics, AI-driven fraud detection, cloud-based POS systems, and innovative self-service technologies, retailers are poised to deliver a more seamless and satisfying shopping journey. While challenges such as infrastructure investment, data security, and consumer adoption remain, the strategic imperative for retail payment innovation is clear. By embracing these advancements, retailers can not only meet but exceed evolving consumer expectations, paving the way for a future where payments are truly frictionless and shopping is an unhindered pleasure.